Interstate Gas Pipeline Paradigm

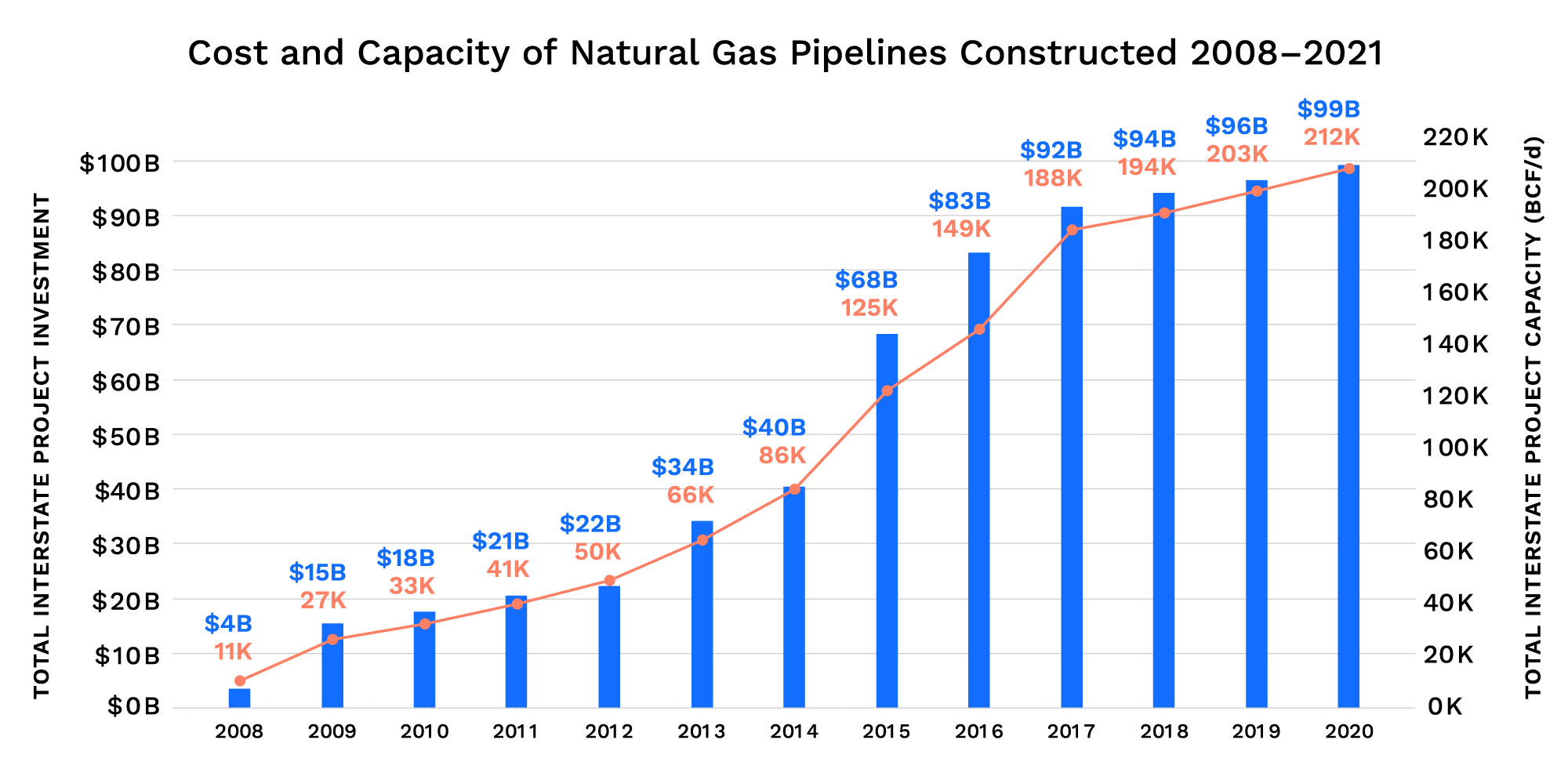

This is in stark contrast to the regulatory and legal paradigm that supported the building of pipeline infrastructure to support the Shale Revolution. That paradigm — based on the 1938 Natural Gas Act and its 1947 amendments — supported the construction of $100 billion dollars and 18,195 miles of interstate natural gas pipelines between 2008 and 2020 that, together, equate to approximately 223 BCF/d of capacity.

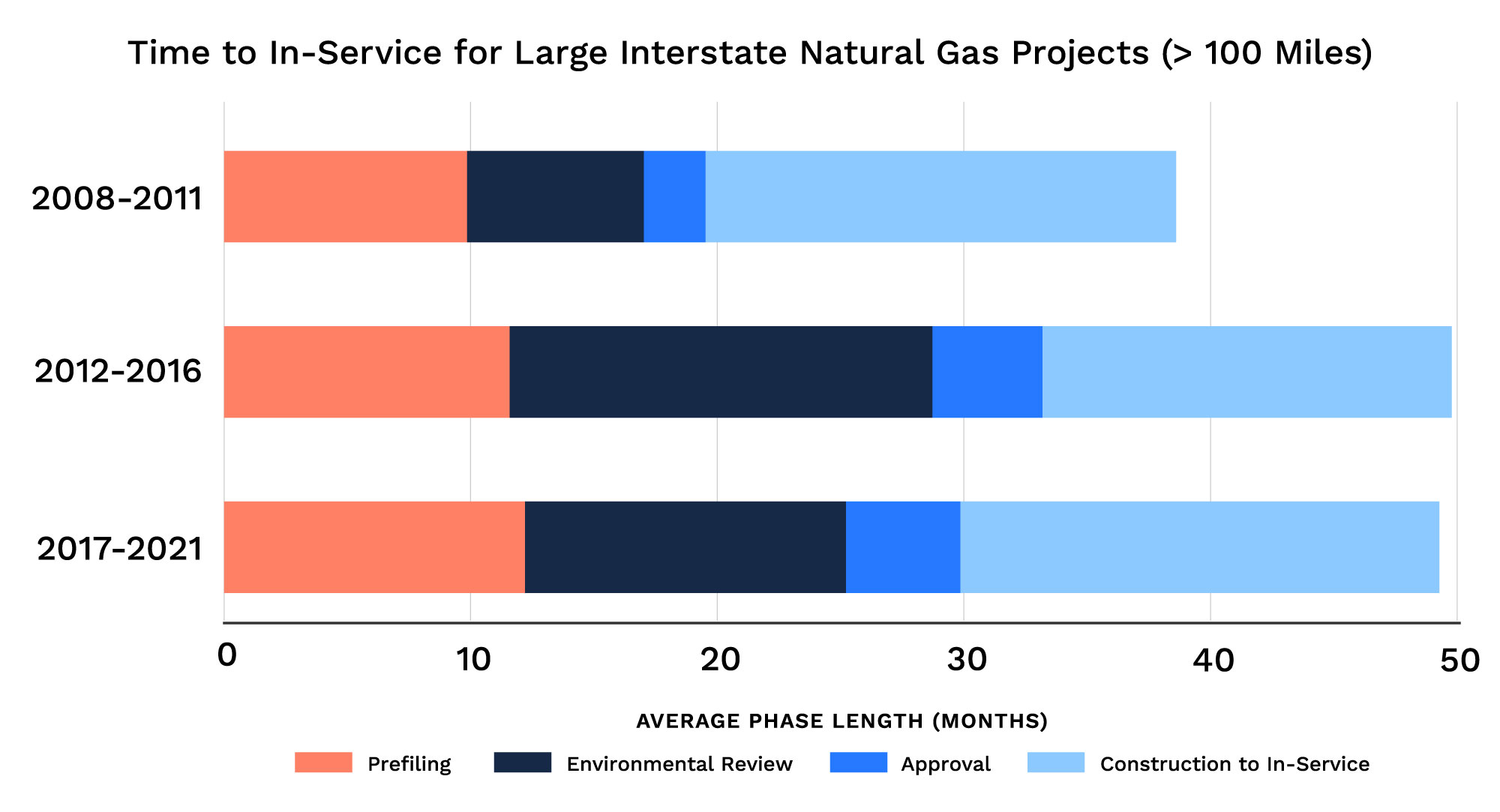

Ninety-seven percent of projects approved under the NGA during that time were approved within two years. The average time for constructing a large (>100 miles) interstate pipeline project from approval to in-service was 3.48 years — well less than a decade for what could be considered linear infrastructure development comparable to electric transmission.

After approval, many projects ran into strong opposition and litigation which dramatically impacted their cost and schedules — and for some, led to cancellation. Two projects, Atlantic Coast Pipeline and PennEast, were litigated all the way to the U.S. Supreme Court, and their cases contain examples of the type of land use and regulatory jurisdictional issues that will most certainly impact future infrastructure projects.

Under the IEA’s proposed path to NZ50, global hydrogen use expands from less than 90 Mt in 2020 to more than 200 Mt in 2030 and to more than 500 Mt in 2050. The most cost-effective way to support this growth by transporting hydrogen is via pipeline, and unlike Europe, the U.S. does not have a plan for the development of a robust hydrogen pipeline network.

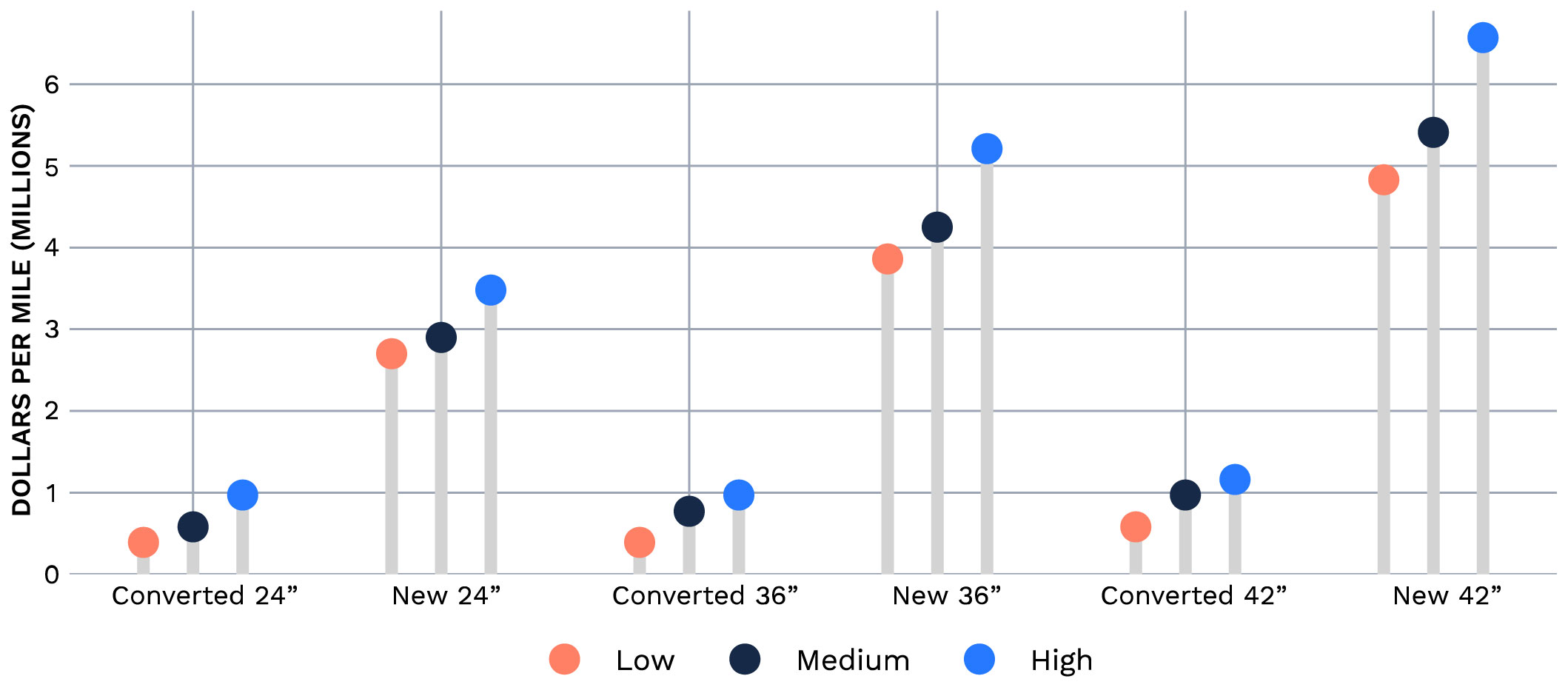

Converting existing natural gas pipelines for hydrogen use presents substantial cost savings versus building new pipelines, ranging from about 10% to as high as 30%. In the European plan, the total cost estimate assumes that 69% of the pipeline network will be repurposed natural gas pipelines and 31% will be new construction.

But here in the U.S., environmental purists are pushing, as the only viable path to net-zero emissions, a plan that requires deep electrification of the entire economy and an almost exclusive reliance on wind and solar to generate that power. By insisting on a single solution and rejecting all other paths, the purists would foreclose participation by existing incumbents in the natural gas industry and the existing gas infrastructure in the transportation and storage of hydrogen as fuel. But more importantly, the insistence on a single solution puts the achievement of the stated goal at risk.

New

Most new generation being built in the U.S. right now is wind and solar, and the bulk of these facilities are fairly small compared to traditional thermal power plants, like natural gas and nuclear.

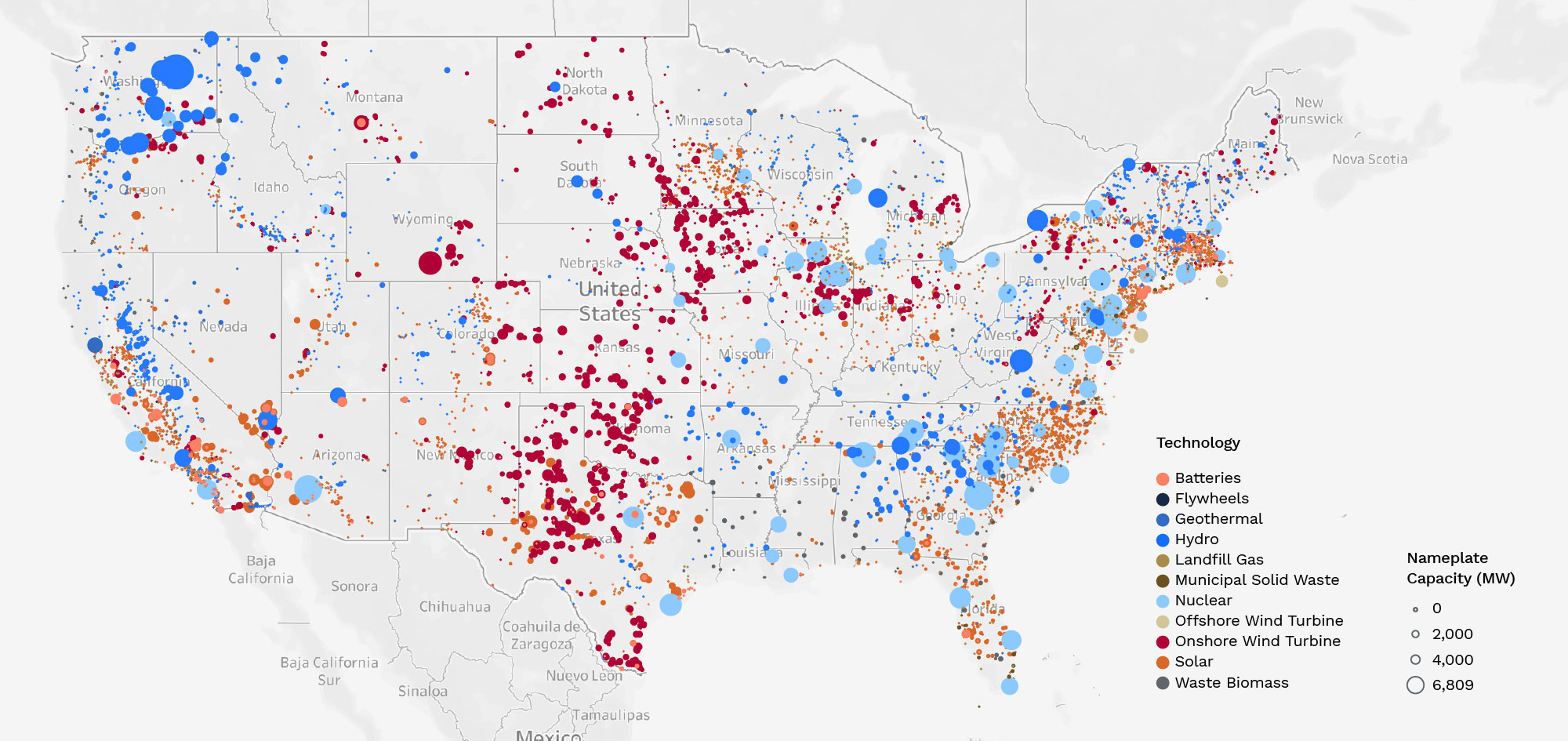

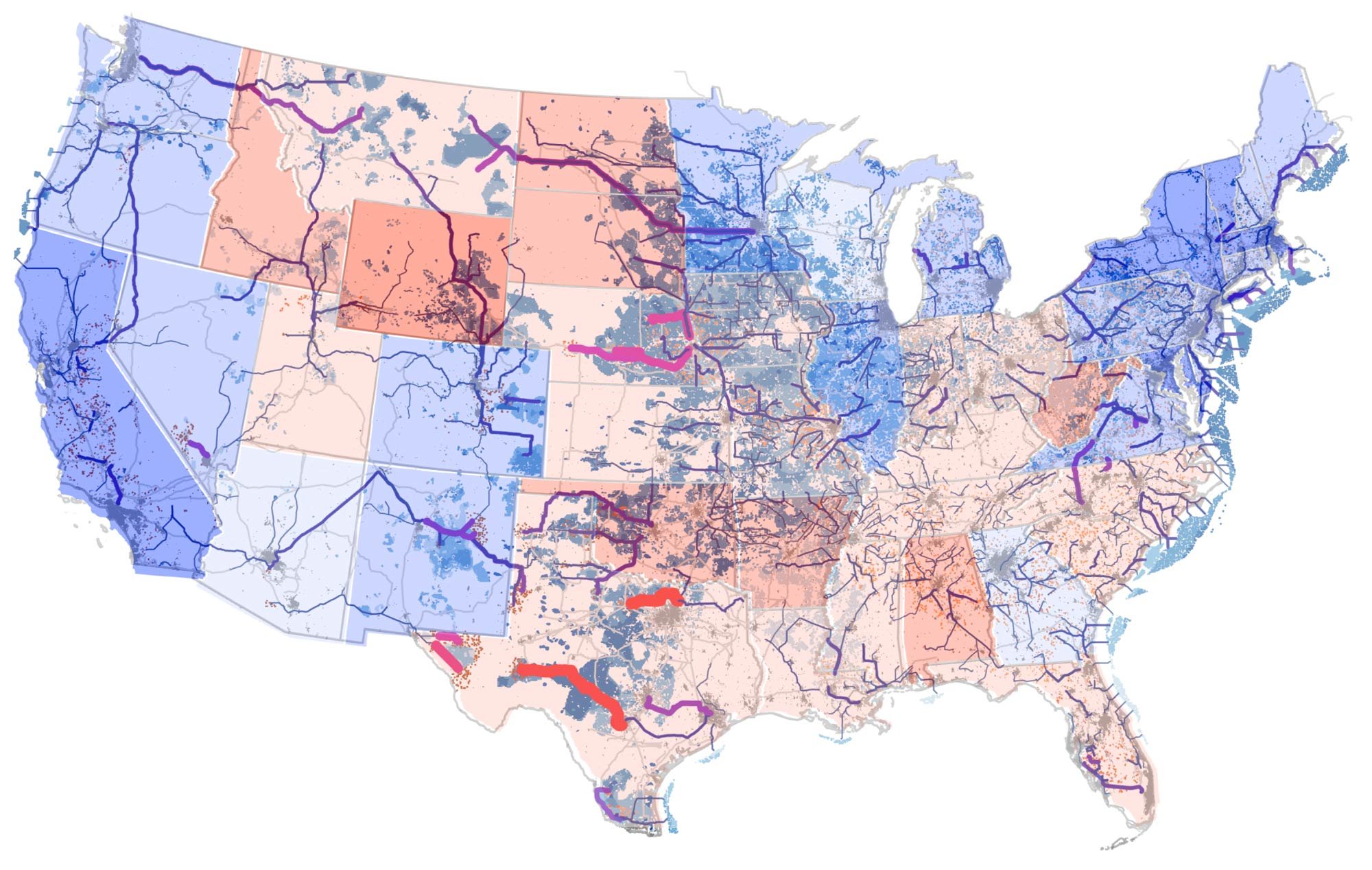

So where are we today on renewable projects useful for electricity generation? We aggregated all the renewable capacity currently in-service and planned projects through 2027 on the map below (an excerpt from Arbo's Renewables Dashboard) — everything from wind to landfill gas. Together it equates to 0.39 terawatts of generation capacity.

The U.S. electric grid delivers more than 3,800 terawatt-hours of electricity to roughly 159 million residential, commercial and industrial end-users each year. So, even if everything on the above map was operational, and could miraculously be running 24 hours a day, 365 days a year, at 2050’s forecasted usage we have 28.2% of the generation capacity needed. Therefore, one can extrapolate that this map needs to be totally filled with colored bubbles to get to NZ50.

Even if we achieve enough renewable generation, we still need to expand our grid by 5.3 times between now and 2050, according to Princeton University’s Net Zero Report. As seen below, this grid will need to be designed to bring wind and solar power from red states to blue states, and must cross a number of states that neither benefit from the new wind and solar construction nor need the power requiring construction of this huge high-voltage grid. The level of polarization in U.S. politics combined with a lack of federal siting authority present potentially insurmountable challenges to achieving this plan by 2050.

Arbo on NPR Marketplace

Gary Kruse, Managing Director of Research, spoke to Kai Ryssdal on NPR Marketplace about these obstacles to NZ electrification in the U.S.

Alternatively, there is an opportunity for entities supporting paths to NZ50 that incorporate robust use of blue and green hydrogen to demonstrate that they can more realistically achieve the goal of net-zero by 2050 in a manner that the International Energy Agency has identified as being the “most technically feasible, cost‐effective and socially acceptable” alternative. The Act’s funding for various hydrogen initiatives is a starting point for the U.S.

Unfortunately for deep electrification proponents, none of the Act’s total $70 billion in energy investment is directed specifically toward increasing renewable capacity or new transmission — just a $2.5 billion loan program for which eligible projects include, but are not limited to, construction of new transmission lines.

Investment & Commerce

Public and Private

Innovation and technologies that create and change industries and markets can require massive investments backed by private capital markets in addition to government financing. Historically, government-funded basic research and development investments — like some set forth in the Act — have led to technology commercialization and associated market development. Sometimes this is a result of serendipitous discovery and sometimes more deliberate industrial policy. The internet is a famous example of this public-private partnership generating innovation, investment and infrastructure.

Notably, Shale Revolution investments were almost entirely comprised of private dollars. Given market dynamics, unit cost economics, and policy-driven origins, this doesn’t seem as likely for “electrification.” Government-directed spending and incentives will be a big part of the required investment, which

has not been addressed in the Act.

Investment Size and Access to Capital

What actually needs to be spent annually and in total to get to NZ50 is not easily or accurately estimable, but here are a few reference numbers from the Business Roundtable:

PJM Interconnection (a Regional Transmission Organization operating from parts of Illinois and Tennessee in the West to the Mid-Atlantic in the East) calculated that reaching 30 percent renewable penetration would require 1,000–3,000 miles of additional transmission lines, at a total cost of $5.0 billion–$13.7 billion.

An estimated $25 billion–$40 billion in additional transmission infrastructure investment is needed through 2025 just to comply with requirements associated with existing state-level renewable portfolio standards.

According to the U.S. Energy Information Administration, U.S. utilities spent $40 billion on transmission in 2019, with about half of that dedicated to new transmission investment. And according to S&P Global, the reconciliation bill currently under Congressional consideration would authorize only $1.5 billion in U.S. Department of Energy grants for new high-voltage transmission projects.

The current landscape finds private capital markets becoming more restrictive. American capitalism historically allocated investments primarily on potential for profitable returns. Now our capital markets have broader stakeholder-driven objectives in areas such as ESG, and activist shareholders significantly influence capital and strategy. There are indications that systemic change is happening and will affect the most needed and impactful investments in innovation and infrastructure.

Larry Fink, CEO of the world’s largest asset manager, Blackrock, made headlines with his 2020 investor letter announcing intentions to exit companies viewed to have high sustainability risks and to require not just those in the energy sphere — but all companies — to disclose their sustainability plans. His 2021 letter expands on these new policies:

“Given how central the energy transition will be to every company’s growth prospects, we are asking companies to disclose a plan for how their business model will be compatible with a net zero economy – that is, one where global warming is limited to well below 2ºC, consistent with a global aspiration of net zero greenhouse gas emissions by 2050.”

The data and methodologies for allocating capital based on NZ50 will likely be problematic. For example, if a diversified energy company has large non-renewables and renewables based businesses and under one public listing, then it may have more difficulty accessing capital markets.

Retail Prices

More restrictive capital markets and the allocation of federal spending are only one constraint or enabler of energy evolution success. A big determinant will be the individual consumer’s willingness to pay a “green premium” and the facilitation of that willingness by rate governing regulators, such as the public utility commissions.

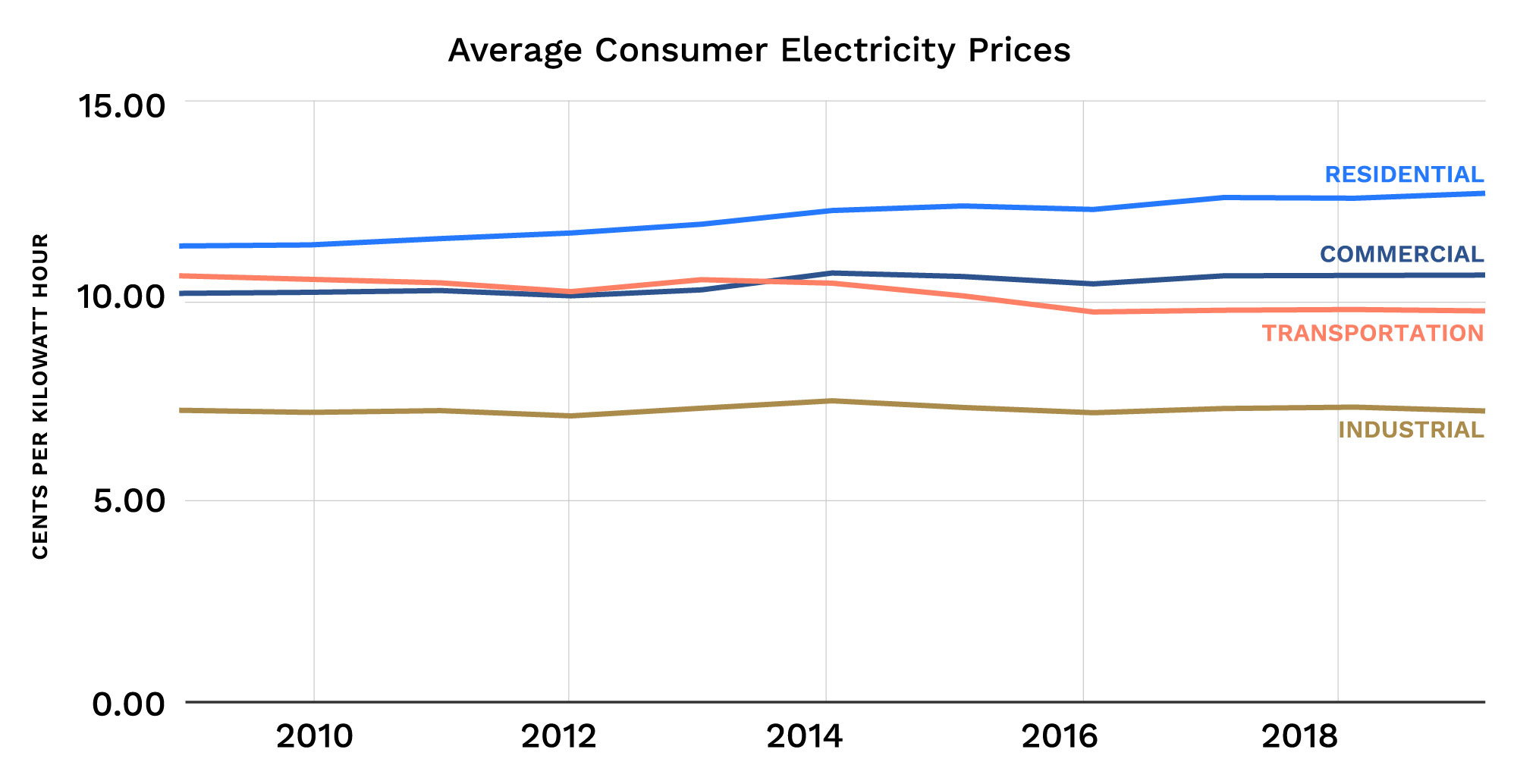

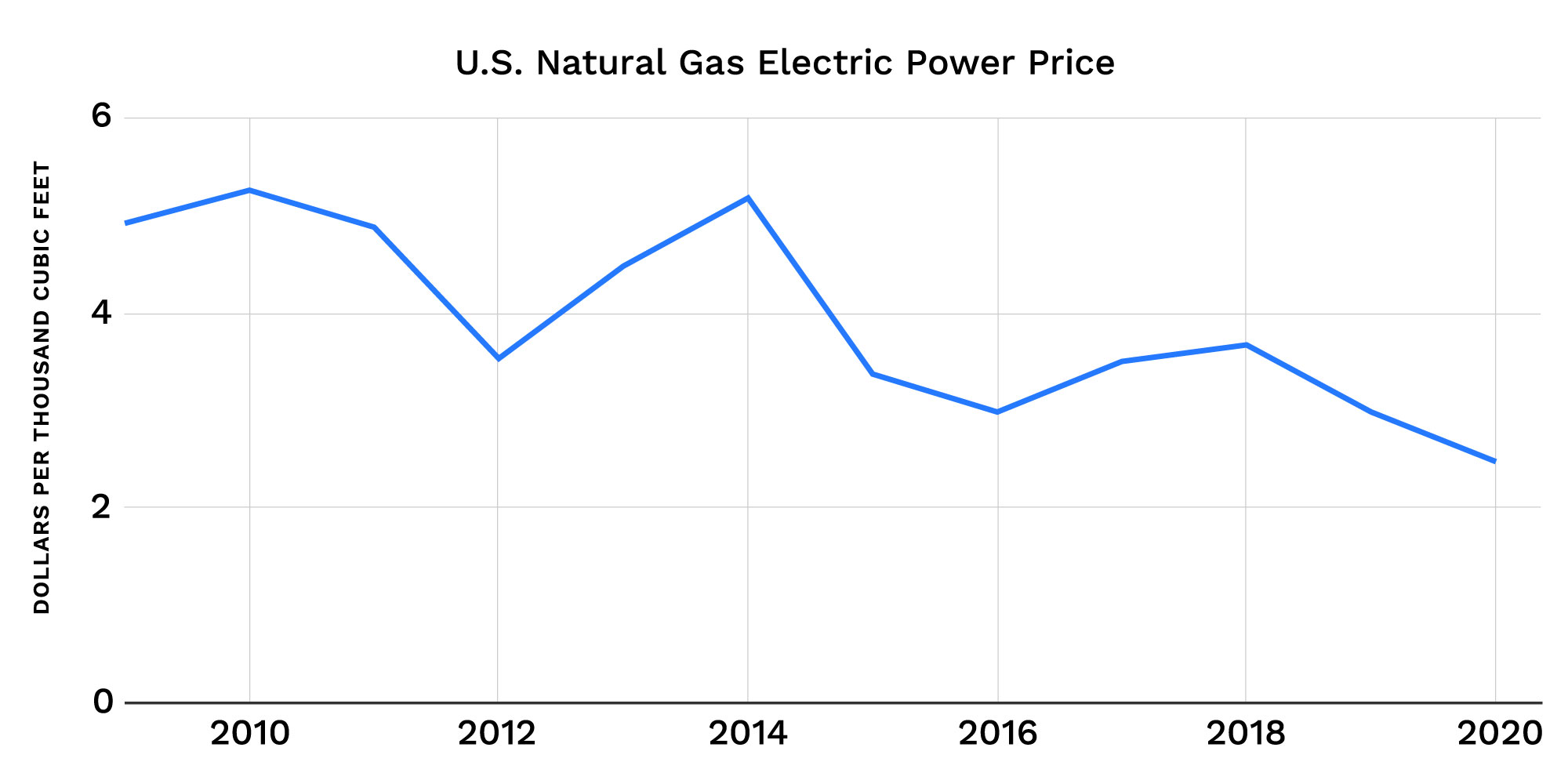

During the Shale Revolution, the U.S. retail consumer did not experience increased prices. As seen in the charts below, electricity prices stayed flat, and natural gas prices for electricity decreased due to abundant supply.

Wholesale Transactions

Most of this report concerns facilitation of the interconnectivity of electrical transmission infrastructure and transportation of energy between supply and demand centers, but facilitation of related commerce will also play a critical role on the road to NZ50. Transactions between wholesale buyers and sellers will need increased efficiency and transparency. Commodities markets include all manner of buyers and sellers from the industrial consumer to large trading houses and brokers to purely financial market makers and speculators.

The complexity of energy commerce is increasing in concert with the expanding number and distribution of energy sources, as well as the need for new pricing mechanisms and markets for instruments such as carbon offsets and products such as responsibly sourced natural gas. This dynamic will challenge wholesale participants’ ability to continuously and transparently access evolving value chains and markets.

Conclusion

The imperative for the world to evolve its production and consumption of energy to combat climate change is clear. Change to the generation, transmission, distribution and consumption of electricity must be a foundation of the energy evolution.

For the U.S. to lead this massive decarbonization effort while maintaining energy independence, it will need to improve its regulatory regimes, foster innovation, make big (bigger) investments, and harness both new and existing infrastructure.